*By Dr David Bell, Specialist Anaesthetist (Retired), Software Engineer, and Founder of Align AI Fitness, NSW, Australia*

In March 2018 I wrote an open letter to Bupa. I posted it on Facebook on a Sunday night and went to bed. By Monday morning it had been shared thousands of times. The Sydney Morning Herald published it later that week.

People still bring it up. So I want to explain what the letter was actually about, what happened afterwards, and why the problem has gotten measurably worse.

What the Letter Said

The letter was about a specific policy change. Bupa announced it was removing its No Gap scheme from all public hospitals. That meant if you were a Bupa member and you were admitted to a public hospital (say, after an accident), Bupa would essentially refuse to pay for your private care in that hospital.

To understand why that matters, you need to understand how the system works.

Let's say a young woman in her twenties has private health insurance. She pays her premiums. She gets her tax rebate and her Medicare levy surcharge exemption. She has peace of mind knowing that if something goes wrong, she is covered.

Then she is in an accident. She badly breaks her leg. She is flown to a regional public hospital and told she needs urgent surgery.

In the emergency room, the hospital clerk asks if she wants to use her private insurance. She says yes. She pays a lot of money for it. Might as well use it. Under the No Gap scheme, she is guaranteed not to be out of pocket.

As her anaesthetist, I take her to theatre. I put her to sleep, intubate her, manage her airway, her blood pressure, her pain. The consultant orthopaedic surgeon comes in from home. Assisted by his registrar, he undertakes a difficult operation that takes three to four hours.

Neither I nor the surgeon is paid by the hospital for that time. We bill her health fund under the No Gap policy. Medicare pays 75 per cent of the scheduled MBS rate. The health fund pays the remainder, plus a small percentage to cover the gap between the MBS rate and the actual cost of care (a gap that had been growing every year since the MBS was frozen in 2013).

Under this arrangement, I earn roughly what the hospital would have paid me. The patient pays nothing. And the public hospital saves money it can spend on other things, like chemotherapy, or keeping alive the man in intensive care with a mysterious septicaemia.

Everyone benefits. The patient, the hospital, the public system.

But Bupa decided to end it. After August 2018, if this woman's insurance was with Bupa, her premiums would still be collected. Her tax rebates would still apply. Her Medicare levy exemption would still stand. But she would have no private care in that public hospital. The consultant surgeon might not come in from home. She might be treated by a less experienced doctor instead.

How could Bupa justify that? How could they expect their members to continue receiving tax rebates and levy exemptions when they would not provide basic hospital cover?

That was the question I asked. And I ended the letter with two sentences: "Your members will suffer. And Australian hospitals will too."

What Happened After

The letter went viral because it said what thousands of doctors were thinking in a way that non-medical people could follow. Patients contacted me. Doctors contacted me. Other health funds contacted me. Journalists contacted me.

The Commonwealth Ombudsman launched an investigation. The Health Minister got involved. The AMA picked up the issue. Politicians raised it in parliament. And by June 2018, Bupa reversed the decision. They created a "Public Hospital Medical Gap Scheme" that restored No Gap cover for public hospital admissions, including emergencies.

That was a win. But it was a narrow one. The reversal fixed the specific policy, but it did not fix the system that made the policy possible in the first place. An insurer had tried to collect premiums while refusing to cover basic hospital care, and the only thing that stopped them was public outrage. Not regulation. Not oversight. A Facebook post that went viral on a Sunday night.

Eight Years Later

I wrote that letter in 2018. It is now 2026. Everything I warned about has come to pass.

The MBS freeze that started in 2013 was partially lifted in 2020, with indexation returning at around 1.5 to 2.4 per cent per year. That sounds like progress until you realise that medical costs (equipment, insurance, staff, rent) have been rising at 4 to 6 per cent annually. The gap between what Medicare pays and what it costs to deliver care has widened every single year, freeze or no freeze. In March 2026, the government ended the 85 per cent out-of-hospital Medicare benefit for over 100 items. The system is not catching up. It is falling further behind.

Gold-level hospital cover (the kind that actually covers major surgery) has dropped from 39 per cent of policyholders in 2020 to 28 per cent by the end of 2025. Over 216,000 policies were downgraded in the first half of 2024 alone. People are not leaving private health insurance entirely (the tax penalties make that expensive). They are downgrading to cheaper policies that cover less.

In April 2026, premiums are going up again. The government approved an average increase of 4.41 per cent. Bupa's increase is 4.8 per cent. For a family paying $5,000 a year, that is another $240 on top of a policy that already covers less than it did five years ago.

Private Healthcare Australia has warned of a "death spiral" where rising costs push younger, healthier people to downgrade or drop cover, concentrating risk among sicker patients, driving premiums higher, pushing more people out. They are describing the exact mechanism I wrote about in 2018. Except now it has a name and actuarial data behind it.

Eighty-two private hospitals have closed since 2020. Private hospitals perform around 70 per cent of elective surgery in this country. When they close, those patients go onto public waiting lists that are already years long. The closures are concentrated exactly where you would expect: regional centres and smaller surgical facilities where the margins were already thin.

And the gap between what patients pay in premiums and what they pay out of pocket keeps growing. The typical out-of-pocket cost for a knee replacement is now around $1,000, with 82 per cent of insured patients paying something for a procedure they thought their insurance covered. The ones who cannot afford the gap do not have the operation. They live with the pain. Nobody counts them.

Where the Money Actually Goes

This is the part that should make everyone angry, and almost nobody talks about it.

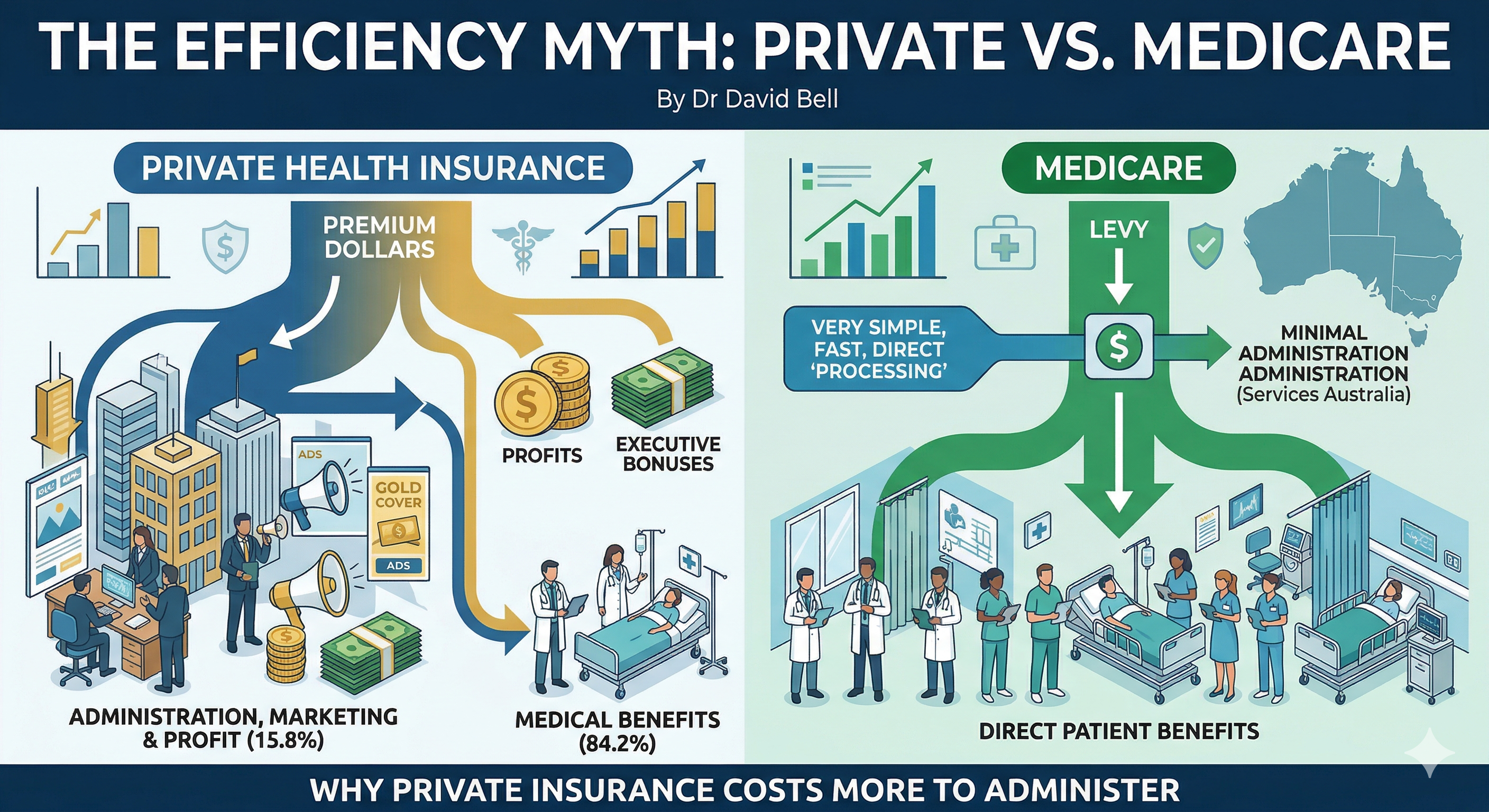

In 2024-25, private health insurers returned 84.2 per cent of premiums to consumers as benefits. That is down from 88 per cent in 2019. It means 15.8 cents of every dollar you pay in premiums does not go to your healthcare. It goes to management expenses, marketing, profit, and executive compensation.

The AMA's 2024 Private Health Insurance Report Card breaks it down further. Over the four years to June 2023, insurer management expenses rose by 32 per cent. Profits rose by 50 per cent. But the amount insurers paid out for medical services during hospital treatment rose by 3.6 per cent. The money is going somewhere. It is not going to patients.

Management expenses alone consumed 10.9 per cent of premiums in 2024-25. The AMA is now calling on the government to mandate that insurers return at least 90 per cent of premiums as benefits. The fact that this needs to be mandated tells you everything.

Now compare that to Medicare. Medicare has no marketing department. No sales teams. No executive bonuses. No shareholder returns. No brand campaigns. No sponsorship deals. It processes claims through a centralised system run by Services Australia. The overhead is a fraction of what private insurers spend, because there is no profit margin built into every transaction.

People repeat the line that the private sector is more efficient than the public sector. In healthcare administration, the opposite is true. Medicare takes your levy, processes your claim, and pays your doctor. A private insurer takes your premium, spends 10.9 per cent on managing itself, takes a profit, and then argues with your surgeon about how much they will pay for your hip replacement.

This is not a left wing argument or a right wing argument. It is arithmetic. And nobody in parliament is making it, because the private health insurance lobby is one of the most effective in the country.

Why It Is So Complicated

Part of the reason nobody talks about this clearly is that Australian healthcare funding is genuinely hard to explain. It is split across three layers, and most people (including most politicians) do not fully understand how they interact.

The first layer is Medicare. Funded by the Medicare levy (1.5 per cent of taxable income, plus a surcharge for high earners without private cover) and general tax revenue, Medicare covers GP visits, specialist consultations, and a percentage of the scheduled fee for procedures. It is Commonwealth money, administered federally.

The second layer is public hospitals. These are owned and run by state governments (NSW Health, Victoria Health, and so on), but jointly funded by the Commonwealth and the states under the National Health Reform Agreement. In 2022-23, public hospital funding was $85.6 billion: 58 per cent from state governments, 37 per cent from the Commonwealth. If you are a public patient in a public hospital, your care is free. But the hospital is funded by both Canberra and your state capital, through a formula that is renegotiated every few years and is a source of constant political argument.

The third layer is private health insurance. This is where it gets messy. Private insurance covers the cost of being a private patient (in either a public or private hospital), and funds about 45 per cent of private hospital revenue. But private hospitals also receive Commonwealth funding through the MBS (when your surgeon bills Medicare for the procedure) and the PBS (for medications). So even in a "private" hospital, the government is paying a significant share.

When Bupa cut the No Gap scheme in 2018, they were pulling one thread in this web. The young woman in the public hospital was being treated as a private patient using her private insurance, which reimbursed the doctors directly, which saved the public hospital money, which freed up state and Commonwealth funding for other patients. Bupa's decision would have broken that chain. The hospital would have had to pay the doctors from its own budget (state and federal money), or the patient would have been treated as a public patient by whoever was on duty.

Three layers of government. One private insurer. One decision. And the people who understand the system well enough to see the consequences are the ones in the operating theatre at 2am, not the ones setting the policy.

What I Would Write Today

If I were writing that letter now, the woman in her twenties would be the same. The accident would be the same. The public hospital, the surgeon called from home, the three to four hours in theatre. All the same.

But the numbers would be worse. I would add the 82 hospitals that have closed. The 216,000 policies downgraded. The actuarial warnings about a death spiral that the industry itself is now using. And I would add the number that should be on the front page of every newspaper in the country: for every dollar you pay in health insurance premiums, 15.8 cents does not go to your care. It goes to the insurer. And that proportion is growing every year.

I am no longer practising anaesthesia. But I was in those theatres for years. I saw what happens when the system works and I saw what happens when it fails. The letter I wrote in 2018 was not a prediction. It was a description of a system already breaking.

Your members are still suffering, Bupa. And Australian hospitals are too.

I wrote a companion piece on the administrative cost comparison between private health insurance and Medicare: The Efficiency Myth: Why Private Health Insurance Costs More to Administer Than Medicare.

The original letter, published in the Sydney Morning Herald: Dear Bupa: Your policy change makes me worry for my patients and for the hospitals in which I work